Soaring volumes, billion-dollar fortunes, insane leverage and radical new risk models: welcome to the wild world of unregulated cryptocurrency derivatives.

The real action in crypto derivatives

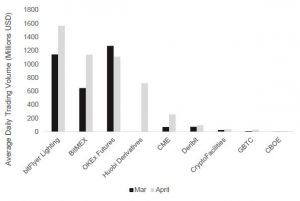

The Chicago Mercantile Exchange (CME), one of the world’s largest established exchanges for derivatives trading, recently recorded a record volume day in bitcoin.

Derivatives are financial contracts that are priced with respect to an underlying reference asset, such as the S&P 500 index, oil or the price of bitcoin.

On 13 May, the CME, a regulated exchange, traded 33,677 bitcoin futures contracts (equivalent to 168,385 bitcoins, or $1.3bn at that day’s exchange rate), 32 times more than the average daily volume during the first month of the contract’s existence, December 2017.

Yet trading volumes on the CME are still dwarfed by those on unregulated derivatives exchanges, many of which operate in the Far East.

In April 2019, according to data provider CryptoCompare, average daily trading volumes on bitFlyer Lightning (headquartered in Japan), BitMEX (Hong Kong), OKEx Futures (Malaysia) and Huobi Derivatives (Singapore) all exceeded those on the CME by between three and five times.

Trading volumes in cryptocurrency derivatives

Source: CryptoCompare

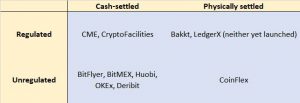

Classifying crypto derivatives

Cryptocurrency derivatives trading platforms fall into four categories. The key dividing lines are whether exchanges are regulated or unregulated, and whether they offer derivatives contracts that settle against a cash benchmark or against physical delivery of the underlying cryptocurrency.

Four types of crypto derivatives trading platform (with examples)

Choosing who you’re dealing with takes a leap of faith

Futures trading—and any trading involving leverage—is particularly risky. Because borrowed money is involved, the default of any market participant could cause a chain reaction, putting the whole system at risk.

So around the world, regulated derivatives exchanges tend to adhere to common risk management standards, such as the use of central counterparty clearing houses (CCPs) to reduce the risk of non-payment by a trader.

But in the less regulated segments of the crypto derivatives market, choosing who to deal with, who (if anyone) supervises them and what risks you might be exposed to takes some investigative work and a leap of faith.

For example, bitFlyer, based in Japan, says on its website that although it calls itself an exchange, it’s not a “financial instruments exchange as defined by [Japan’s] Financial Instruments and Exchange Act”.

Huobi, which moved its head office from China to Singapore in 2017, says it offers a “trading platform of professional and international standards for the majority of global digital assets enthusiasts and investors, on the precondition that it does not violate any of the relevant laws and regulations of the British Virgin Islands”.

BitMEX, which last year rented the most expensive office space in the world (in Hong Kong), says it aims to comply with the anti-money laundering and corporate laws of the Seychelles, where its parent company is incorporated.

The race for physical settlement

Many of the most popular existing cryptocurrency derivative contracts settle in cash against an index based on spot prices. A spot price—as opposed to a forward or future price—is the price for the immediate settlement of a transaction.

For example, at their regular expiry dates, the CME’s bitcoin futures contracts settle in cash against a reference rate developed jointly by the CME and Crypto Facilities, called the Bitcoin Reference Rate (BRR).

If cash settlement is used for a derivatives contract, there’s always the risk of someone in the market seeking to push prices in their favour at the moment the settlement price is determined.

So to avoid the likelihood of LIBOR-style benchmark manipulation at the regular expiry dates of their bitcoin futures contracts, the CME and Crypto Facilities put in a number of safeguards.

For example, the BRR aggregates the trade flow of four major bitcoin spot exchanges during a specific one-hour calculation window, rather than relying on a single price feed at a single point in time.

And to further reduce the risk of manipulation, this one-hour window is partitioned into 12 five-minute intervals. The BRR is then calculated as the equally-weighted average of the volume-weighted medians of all 12 partitions.

But some popular unregulated cryptocurrency derivatives don’t settle at all. For example, BitMEX’s most widely traded product is a perpetual bitcoin contract.

The contract, says BitMEX, mimics a margin-based market for continuous trading in bitcoin’s spot price.

Perpetual contracts trade at close to the underlying market price for bitcoin, says BitMEX, because of a funding mechanism that requires long and short contract holders to exchange payments every eight hours.

Physical settlement of a derivatives contract is the preferred option

However, there’s also a race to develop physical settlement mechanisms in cryptocurrency derivatives.

For many traders, the physical settlement of a derivatives contract is the preferred option: most notably, physical settlement eliminates the risk of the price at a contract’s settlement diverging from the prevailing market price.

However, physically settled bitcoin derivatives have been slow to arrive, largely due to concerns about managing the custody risk that is inherent in cryptocurrencies.

One widely publicised project by Bakkt, which is supported by Intercontinental Exchange (ICE), the owner of the New York Stock Exchange, has been repeatedly delayed in its launch plans.

In February this year, the Commodity Futures Trading Commission (CFTC), the federal regulator of the US futures markets, told Bakkt that if it wanted to take custody of bitcoin—a prerequisite for anyone offering physically settled derivatives—it would need to go through additional steps to gain approval for launch.

In the US financial markets, asset custody is regulated at the state level, while futures are supervised country-wide by the CFTC.

In April, ICE announced that it had bought a digital asset custodian to help develop its physically backed bitcoin futures.

Bakkt says it is due to start test trading in bitcoin futures next month, while another US company, LedgerX, is also apparently making progress with regulators from the CFTC.

However, not all cryptocurrency derivatives exchanges with physical settlement plans want to go down the Bakkt/LedgerX route of full compliance with futures regulation.

CoinFLEX, a Hong Kong-based exchange, which launched trading earlier this year, says it is providing physical settlement while staying unregulated.

The exchange says it’s focused on the Asian retail market and cryptocurrency-focused institutions, such as mining firms, OTC trading desks and proprietary trading firms.

CoinFLEX is registered in the Seychelles, but says it will be fully compliant with know-your-customer and anti-money laundering rules.

100 times leverage

Futures trading is about leverage. But here there’s little in common between regulated and unregulated cryptocurrency derivative trading venues. And some exchanges permit what can only be termed an extreme form of gambling.

The margin requirements of the CME, the largest regulated futures exchange for bitcoin, limit exposure to around two times the minimum outlay of margin.

But in the unregulated cryptocurrency derivatives market, much higher levels of leverage are possible.

“It’s completely insane you can get 100 times leverage”

For example, BitMEX permits those opening a perpetual swap position to gain exposure of up to 100 times the initial outlay.

Bitfinex, a cryptocurrency exchange that’s recently been the subject of accusations of fraud from New York’s Attorney General, is also aiming to get into high-risk trading. The exchange says it’s about to launch a trading product with 100 times leverage.

Some cryptocurrency market participants query the wisdom of allowing retail punters access to such levels of gearing, which offer a very high chance that a position will reach a risk limit and be liquidated, particularly in such a volatile asset class as cryptocurrency.

“It’s completely insane that you have implied volatility on bitcoin of 90 percent and you can get 100 times leverage,” said Alexi Esmail-Yakas, head of product at Elwood Asset Management, speaking at the recent CryptoCompare Digital Asset Summit in London.

Some jurisdictions have already cracked down on online platforms that encourage such risky trading. Last year the European Securities and Markets Authority (ESMA), Europe’s financial markets regulator, prohibited the sale to retail clients in the European Union of any cryptocurrency derivatives product offering more than two times leverage.

ESMA said it had found that around nine in ten of the retail investors that use leveraged trading platforms end up losing their money.

Some trading platforms say they respect these rules.

“As an FCA-regulated provider, we abide by the guidance from the European Securities and Markets Authority (ESMA),” said Sui Chung, head of cryptocurrency pricing products at Crypto Facilities, which was purchased earlier this year by cryptocurrency exchange Kraken.

“On our platform, retail investors are limited to two times leverage,” Chung told New Money Review.

“But for unregulated, undocumented trading venues, those constraints don’t exist.”

Elwood Asset Management’s Esmail-Yakas suggested that the interests of high-leverage trading platforms are not aligned with those using them, and that the potential revenues from facilitating speculation outweigh concerns over client safety.

“When the Swiss peg against the euro broke a few years ago, retail investors got burnt with much lower levels of leverage than in bitcoin derivatives,” said Esmail-Yakas.

“But it’s an incredibly profitable line of business for BitMEX.”

Minting billionaires

BitMEX, along with other unregulated crypto exchanges, doesn’t disclose its revenues.

These can be substantial. Cryptocurrency derivatives trading platforms could make money in a number of ways: for example, from trading fees, which are likely to be multiplied if high leverage causes traders to have their positions liquidated on a regular basis.

“BitMEX’s perpetual swap will go down in history”

But the revenues of cryptocurrency derivative exchanges can still be inferred from some of the personal fortunes they are generating.

Last year, the Times reported that one of the co-founders of BitMEX, Ben Delo, had become a billionaire in the space of four years.

The Times wrote that mathematician and computer scientist Delo, who is 35, had been voted by contemporaries at his Oxford college as the student most likely to become a millionaire—and the second most likely to end up in prison.

Some market participants praise the unregulated cryptocurrency exchanges for their spirit of innovation.

“BitMEX invented the perpetual swap. It created a market that wasn’t even there. It will go down in history as a financial product that allowed many people to enter the derivatives market that would never otherwise have been able to,” Manny Alamu, European head of business development at CoinFlex, told New Money Review.

However, Alamu cautioned that the contract is only designed for short-term speculation.

“There are downsides to BitMEX’s product, which people are only starting to see now—the implied funding rate can be very expensive and the perpetual swap has negative convexity,” said Alamu.

Negative convexity means that the profit/loss position of a perpetual swap position does not change in a linear fashion with a change in the underlying bitcoin price: instead, profits accrue less quickly as the market moves in your favour, while losses compound faster, the further the market moves away from you.

Socialised losses: an alternative to central clearing

In the traditional futures market, a clearing house (CCP) underwrites the risk of a default of one of the brokers trading on the exchange or, indirectly, the risk of a default of one of the broker’s clients.

This is because the CCP interposes itself between all buyers and sellers on the exchange, acting as the seller to every buyer and the buyer to every seller.

The no-default promise is backed up by several layers of defence: money posted to CCP as margin by both parties to a trade; a default fund to which all clearing members contribute; and, ultimately, by the CCP’s own capital.

The guarantee is not foolproof, however. CCPs have failed in the past by running out of money when leveraged traders went bust.

But CCPs are now a critical part of the financial infrastructure. And particularly since the 2008 financial crisis, regulators have placed extra importance on building the derivatives market around a central clearing model.

Given their importance in the financial system, CCPs have been labelled “super-systemic” and too important to fail. There’s an unspoken understanding that if a larger CCP gets into trouble, taxpayers are likely to be called on to bail it out.

In the unregulated cryptocurrency derivatives market, trading takes place on a peer-to-peer basis and, by definition, there’s no such thing as a CCP.

However, many cryptocurrency derivatives exchanges have embarked on a risk management model that carries its own form of mutualisation.

Instead of the clearing house regime of relying on several lines of defence to ward off defaults, some cryptocurrency exchanges explicitly promise to share any losses incurred from defaults with exchange users.

“Winners need to make a contribution to cover the losses of the losers”

How does this work? On a peer-to-peer crypto derivatives exchange, traders have exposure to each other, rather than to a central risk management entity like a CCP.

And when a leveraged trading position starts to move against one participant in a bilateral trade, depleting their maintenance margin, the crypto derivatives exchange steps in and automatically liquidates the losing position.

However, in fast-moving markets, the liquidation may take place at a worse price than the point at which the losing trader has run out of margin.

This leaves the winning trader (the person with the opposing position) with a potential shortfall.

Cryptocurrency derivatives exchanges have therefore set up insurance funds to compensate traders with winning positions in the event that the margin payments of losing traders prove insufficient.

As at 25 June, BitMEX’s insurance fund, for example, stood at 28,332 bitcoin, worth around $360m.

However, the insurance fund concept has its limits.

As BitMEX made clear in a blog published earlier this year, in the event that the insurance fund itself runs out of cash, winners cannot be confident of taking home as much profit as they are entitled to.

BitMEX says that its insurance fund has been fully depleted in the past, for example when the bitcoin price fell 30 percent in five minutes in March 2017.

That sharp move occurred when the Securities and Exchange Commission said it was refusing an application by the Winklevoss brothers to launch a bitcoin exchange-traded fund (ETF).

One competing exchange says it has not run into such problems.

“On our exchange we never had a socialised loss event,” Deribit, a futures and options exchange run out of Amsterdam, told New Money Review.

Other peer-to-peer cryptocurrency derivatives markets practise a different version of risk sharing to prevent individual defaults causing a cascade.

“On Crypto Facilities we don’t allow anyone’s trading position to fall into negative equity,” Sui Chung told New Money Review.

“We don’t supply credit and there are no such things as margin calls. Traders have initial margin and maintenance margin. Once the maintenance margin is breached your position is liquidated,” said Chung.

“We then have a system of assignments: if your maintenance margin is breached, your contracts are novated to another member, who will take over the positions and ensure the system remains robust.”

“Those receiving assignments get an economic reward in the form of a difference between the price at which the position is assigned and the price at which all the collateral is exhausted (at which there is zero equity),” said Chung.

The ethos of crypto

So in large parts of the cryptocurrency derivatives market, default risk is not delegated to a CCP and (largely) forgotten. Instead, it’s seen a condition of doing business with the exchange itself.

“The traditional clearing model is operated by very large institutions with very large balance sheets,” Chung told New Money Review.

“That model also involves brokers and the extension of credit. In a sense it’s more user-friendly: if your margin is used up, you get a call from your broker and the chance to post more collateral, before having your positions closed out. You also have the chance to cross-margin different positions, generating capital efficiencies.”

Asked about the pros and cons of the central clearing model versus the tendency to socialise losses at unregulated exchanges, the CME pointed out what it sees as its own model’s advantages.

“Overall, offering a futures contract on a regulated marketplace brings a number of benefits to market participants, including transparency, price discovery and risk transfer – all of which better enable them to manage their risk as the bitcoin market develops”, Tim McCourt, CME’s group head of equity index and alternative investment products, told New Money Review.

“We have put in place risk mitigation tools such as margin, credit controls and price limits to appropriately manage the risk of listing and clearing bitcoin futures,” said McCourt.

But non-cleared cryptocurrency derivatives, says Crypto Facilities’ Sui Chung, embed one of the main principles of the technology launched a decade ago with the appearance of bitcoin: it must be able to survive without central control.

“Under our model, the onus is on the individual trader to manage exposure and ensure that there is sufficient collateral to keep the position alive,” said Crypto Facilities’ Chung.

“In a sense, the model reflects the ethos of crypto: it’s your asset, look after it yourself, there are fewer intermediaries, there’s less trust baked in,” he said.

[Correction: in an earlier version of this article we reported that BitMEX earns money from the funding rate charged to longs and shorts in its perpetual bitcoin contract. In fact the funding rate charges are set purely peer-to-peer]

Don’t miss any more New Money Review content: sign up here for our newsletter

Support New Money Review on Patreon or by donating in cryptocurrency